Archive

Nickel Mining in North America: It's a US National Security Issue

| |||||||||

|  |  |  |  | |||||

January 23, 2025 – TheNewswire – Burlington, Ontario - By 2030, demand for battery-grade nickel is projected to triple, driven largely by production of electric vehicles (EVs) in the West.

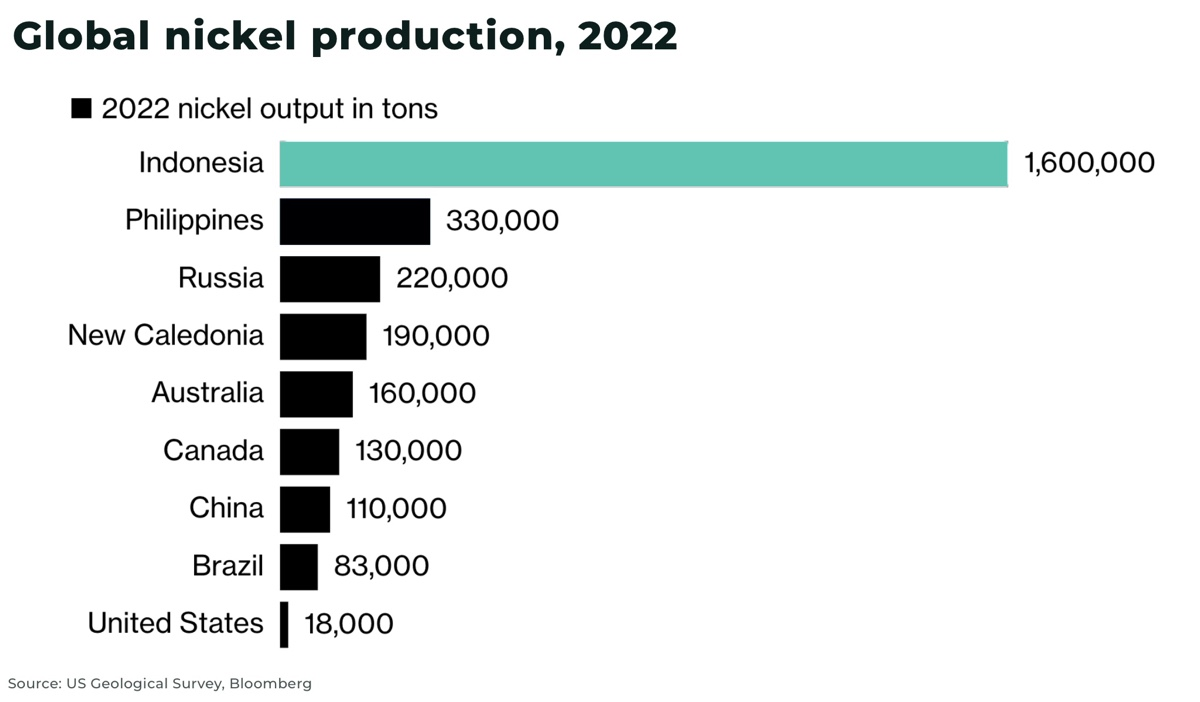

The challenge for Western economies is that Indonesia, with the support of China, dominates global nickel production:

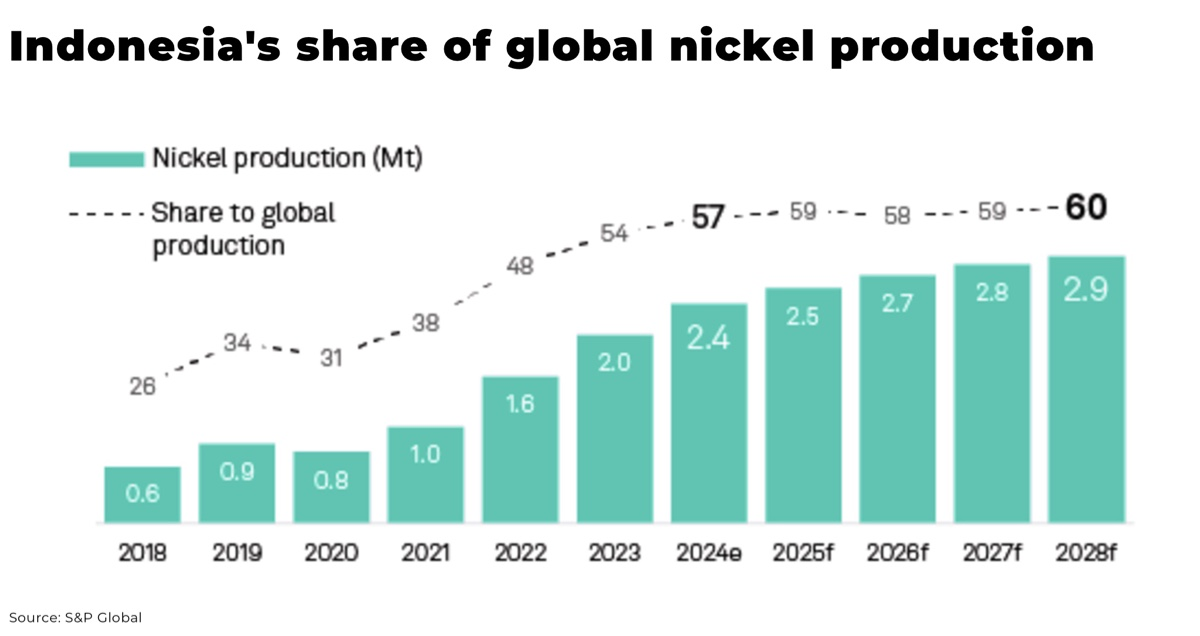

54% of mined nickel supply coming from Indonesia in 2023

Indonesia forecast to represent more than 60% of global supply by 2028

Concerns that Indonesia may use this market dominance to gain economic and geopolitical leverage intensified when an international trade war was launched over nickel in 2024.

Without access to secure supply of nickel, North America's production of electric batteries is not secure — and it's not just about EVs, but defence, the energy transition, and more.

Click Image To View Full Size

Nickel

Nickel is listed as a critical mineral in the US for good reason, essential for:

-

EVs

-

stainless steel

-

aerospace and defence

-

AI and data centers

-

the energy transition and nuclear power

Electric batteries

In particular, the importance of nickel to the energy transition cannot be overstated, especially as a critical component in electric batteries, enhancing their energy density and overall performance.

-

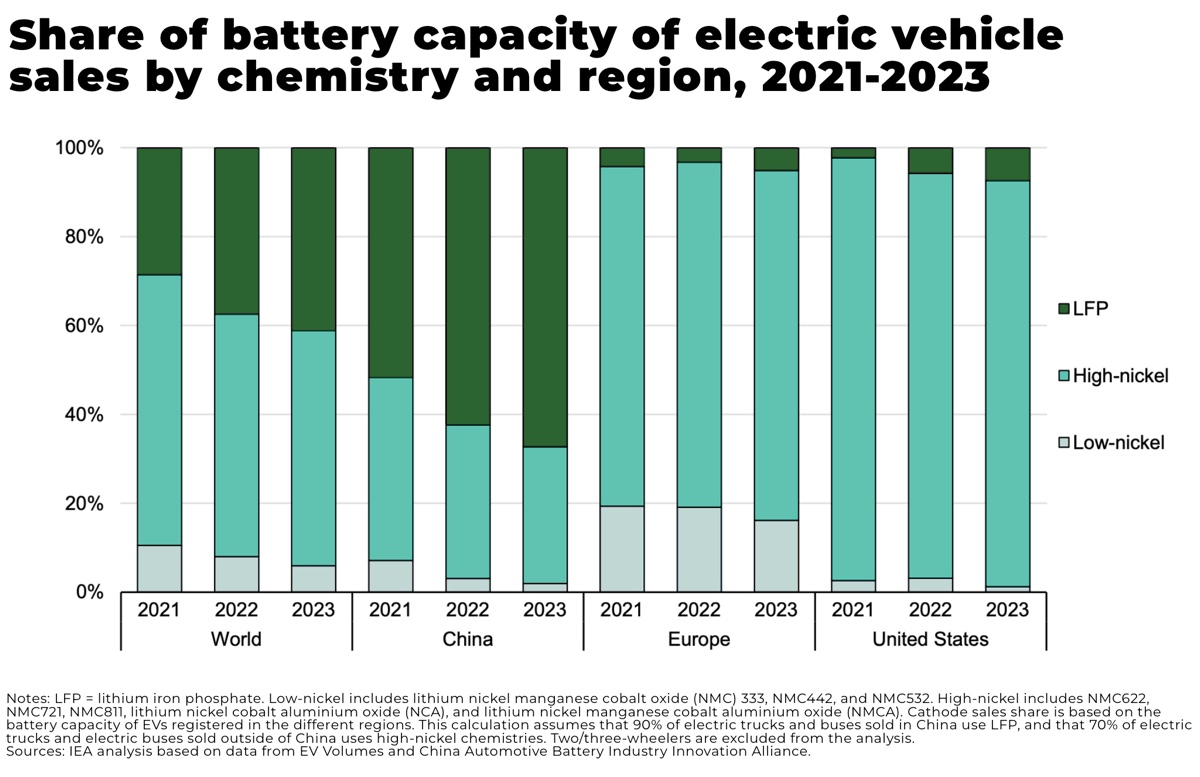

over 50% of batteries, produced in 2023, use chemistries with relatively high nickel content

-

electric battery demand for nickel stood at almost 370 kt in 2023, up nearly 30% compared to 2022

-

China has increased its use of lithium-iron-phosphate (LFP) chemistry in batteries, but the share of LFP batteries in the US and Europe is below 10%, with high-nickel chemistries still most prevalent

There are alternative electric battery chemistries that do not use nickel, for example, China has increased its use of lithium-iron-phosphate (LFP) chemistry in batteries, but in North America and Europe the share of LFP batteries is below 10%, with high-nickel chemistries (eg nickel-manganese-cobalt-oxide (NMC)) still most prevalent.

Benchmark Minerals projects that nickel-based chemistries will capture 85% battery cell production capacity outside of China by 2030. Electric batteries are forecast to account for over 50% of nickel demand growth by 2030, reaching 1.5 million tonnes of nickel demand by the end of the decade.

“There will be growth in China, but it won’t be as pronounced as in ex-China markets”

— Jorge Uzcategui, senior nickel analyst at Benchmark

Click Image To View Full Size

And, even if the electric battery chemistry in the West can also push the nickel content down, demand is still expected to rise as sales of electric vehicles increases.

The Great Nickel Trade War

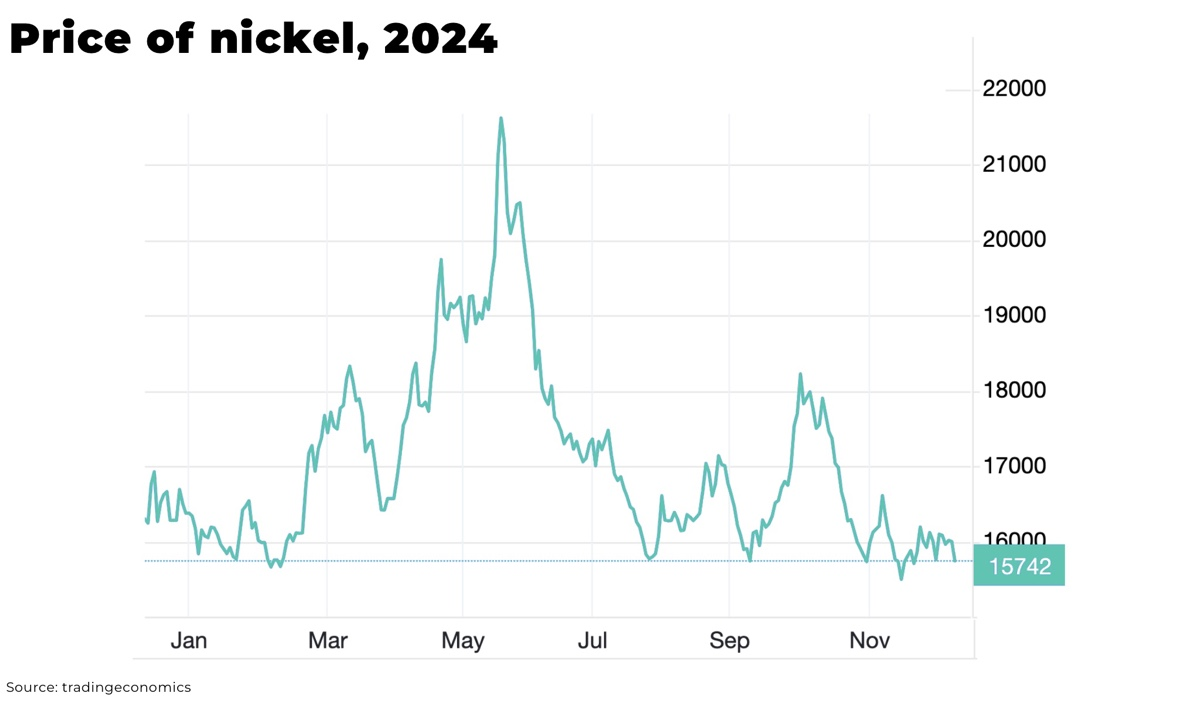

Nickel is at the centre of a global trade war over market share, with Indonesia forcing the price down by more than 50% since the recent peak in December 2022 to take out Western competitors.

Click Image To View Full Size

As we highlighted in our recent analysis — the Great Nickel Trade War — the list of nickel mines closing is growing longer, especially in Australia, with at least 8 mothballing operations.

Indonesia is working to monopolise its market dominance of the nickel supply chain, from mining to refining to electric battery production.

This obviously makes Indonesia's position even stronger in the global supply chain.

“If we see a lot of non-Indonesia projects go to the wall, then Indonesia’s share goes even higher. At the moment, there is no alternative. There is no big source being developed or approved elsewhere”

— according to Jim Lennon, commodity strategy consultant at Macquarie Bank

Western companies are investing into Indonesia, for example, Ford Motor has taken a direct stake in a battery-nickel plant worth US$4.5 billion.

However, the concern in the West is, what happens if Indonesia wants to leverage its influence of these markets further, for example, as China has recently done with its ban of antimony, germanium and gallium to the US.

And, to note, China has been instrumental in developing Indonesia's nickel industry, with 54% of the country's nickel output in 2023 coming from China majority-owned producers.

Outside of Indonesia, Indonesia is also now importing ore from the Philippines for refining, equivilent to 3% of supply.

It’s estimated US FTA partners account for only 9.3% of global nickel production, without any of the top three exporters (Indonesia, the Philippines, and Russia).

Click Image To View Full Size

Trump making mining great again

The Biden administration introduced a US$7,500 tax credit for new EVs available under the Inflation Reduction Act, available only if the vehicle is built in North America and at least 50% of its battery mineral content sourced in North America or a domestic trading jurisdiction (Indonesia does not have a free-trade agreement with the US, and we do not expect one anytime soon)

Donald Trump has said he wants to scrap the IRA EV tax credit, but his priorities remain the same: to secure vulnerable US supply chains.

So, how to do this?

Domestically:

-

Eagle Mine, the only operating nickel mine in the US, has recently extended its mine-life to 2029

-

the US Department of Defense (DoD) has announced US$20.6m in funding for the development of a proposed Talon nickel mine in the northern state of Minnesota

However, Eagle mine produced 17,000 tons of nickel in 2023, which is not enough to make up for the more than 159,000 tons of imports that year. And, until any permitting reform is done, new mines in the US can take up to 29 years (the second longest timeframe in the world).

Instead, with 46% of US nickel imports coming from Canada in 2023, which accounts for 4% of global production, one of the most secure and likely options will be to leverage the natural resources north of the border.

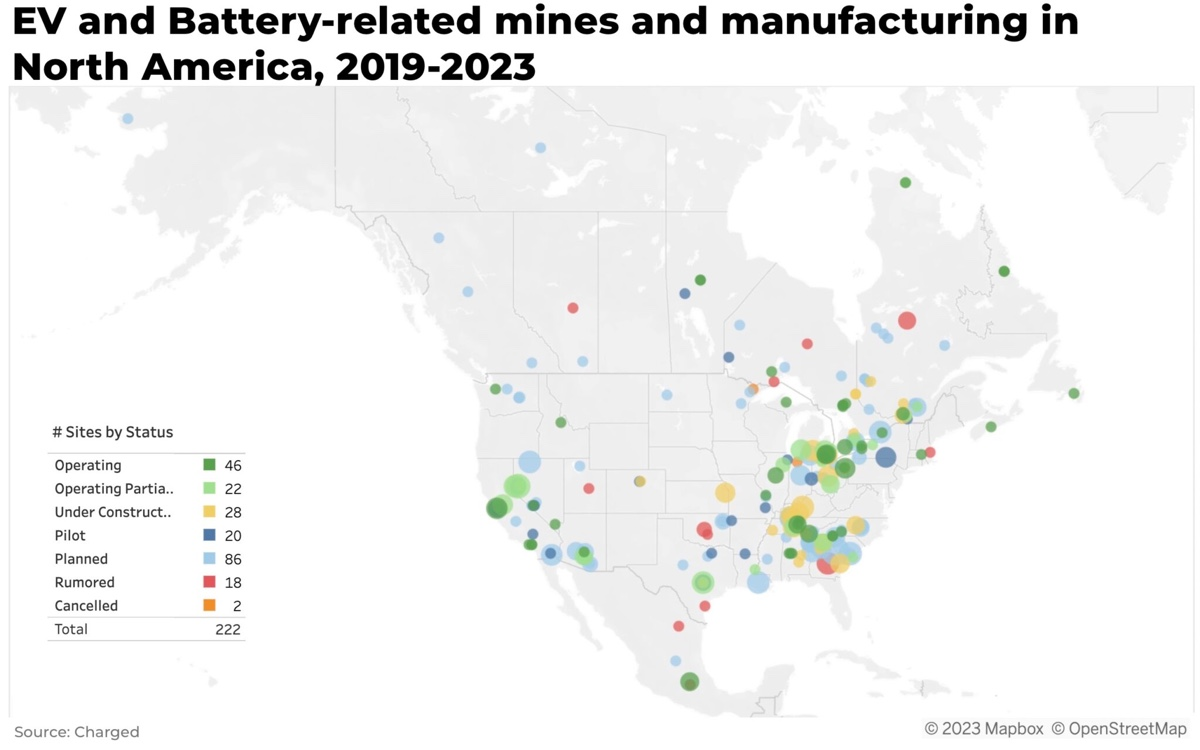

Below is a map of electric battery-related mining projects planned, operating across North America. Note, the concentration of mines in Quebec and Ontario.

Click Image To View Full Size

Now, let’s overlay the EV and battery-related manufacturing and processing plants operating and planned.

Click Image To View Full Size

To support the integration of Canadian mines into the America battery belt, both Canada and the US are strengthening ties across the industry, for example:

-

the Canadian government has started to restrict foreign owned investments in the critical minerals sector, particularly affecting Chinese investments. The provinces are also looking into ways to shorten permitting times

-

the US Defense Department awarded US$14.8 million to two Canadian companies to mine and process critical minerals in North America

The US Defense Department investment comes with “no strings attached,” Energy Minister Jonathan Wilkinson has said, “The only string attached is that we all want to see these companies actually move faster.” -

in 2022, the US announced US$250 million in Defense Production Act (DPA) funding for US and Canadian companies to mine and process critical minerals for electric vehicle and stationary storage batteries

The two largest nickel mines in Canada are operated by Glencore (Raglan and Sudbury Area mines), then third and fourth largest by Vale (Voisey’s Bay mine and Coleman mine).

But current nickel mining capacity in North America is not enough to meet the tripling of demand that is forecast.

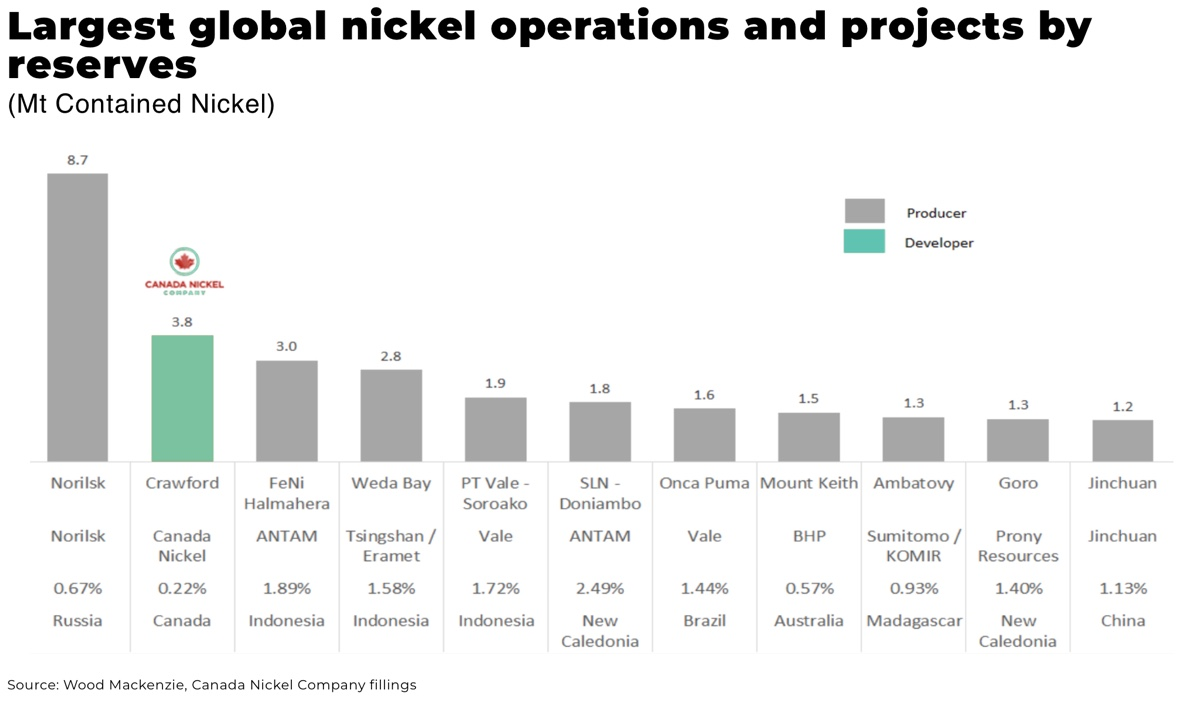

New exploration projects, like Canada Nickel (TSXV: CNC, OTCQX: CNIKF), are working to meet this new expected surge in demand.

Canada Nickel boasts the largest nickel deposit in North America and are positioning themselves for Canada Nickel a global nickel market they believe is “fundamentally short of nickel in medium and long-term – little to no supply growth outside Indonesia/China.”

Click Image To View Full Size

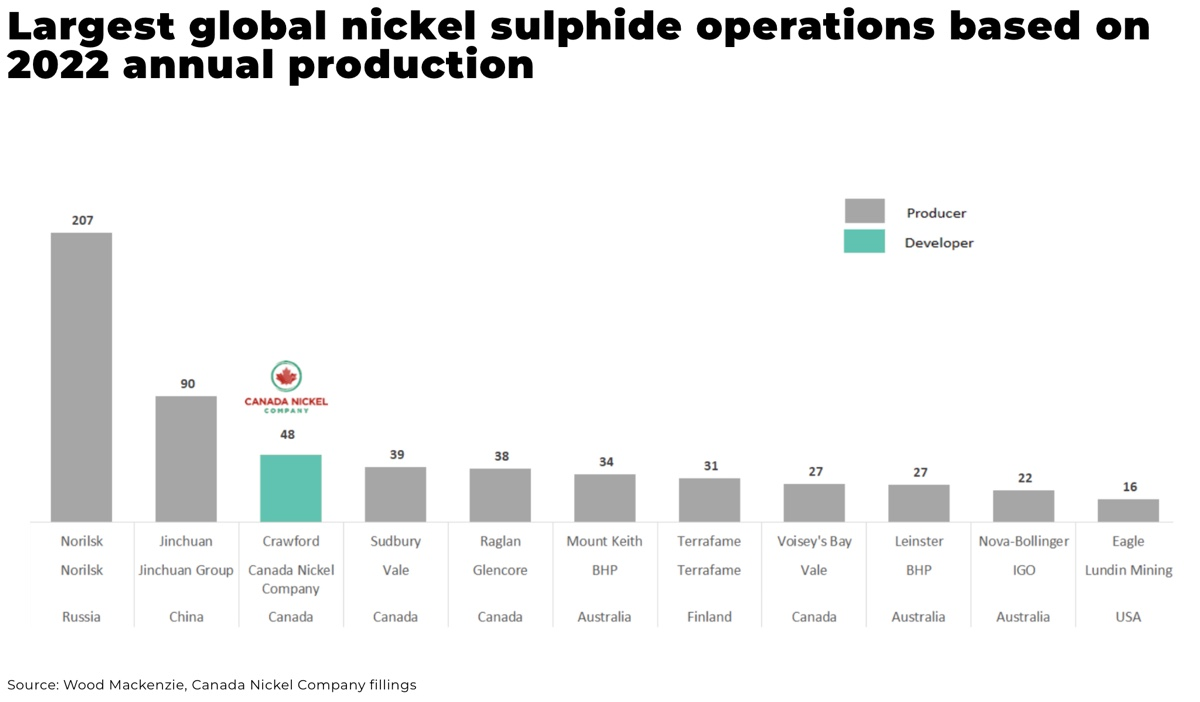

Based on bankable feasibility study results, Crawford is expected to be the 3rd largest nickel sulphide operation globally.

Click Image To View Full Size

As public concerns mount over the environmental impact of mining in Indonesia, and governments and automakers push for responsibly sourced nickel, Canada Nickel is positioning itself as a market leader in sustainable nickel after just secured a US$20million investment from Ontario's First Nations (believed to be the first Indigenous funding into the Canadian critical-minerals industry).

"The Crawford Nickel Project represents a strategic opportunity to secure a stable, ethically-sourced nickel supply for the United States. As the largest nickel deposit in North America, it's poised to become a cornerstone of the continent's critical mineral production. Our commitment to zero-carbon nickel production aligns perfectly with the urgent need for sustainable materials in the electric vehicle and renewable energy sectors.

By developing this resource in Canada, we're not just meeting market demand; we're strengthening the national security of the entire North American continent by reducing reliance on geopolitically sensitive supply chains."

— Mark Selby, CEO of Canada Nickel

Securing America's future: key players in North America's nickel mining supply:

Vale (NYSE: VALE), the Brazilian mining giant, is a major player in the North American nickel market. With significant operations in Canada, including the Voisey's Bay Mine in Newfoundland and Labrador and the Sudbury operations in Ontario, Vale is investing heavily in the region.

The company recently completed a US$2.94 billion expansion project at Voisey's Bay, transitioning from open-pit to underground mining and boosting annual nickel production to 45,000 tons.

Glencore plc (LSE: GLEN | OTC: GLNCY) is a key player in the North American nickel sector, with significant operations in Canada. The company owns the Raglan Mines in Quebec and the Sudbury Area Mine in Ontario, which are among the largest nickel producers in the country.

Glencore's Raglan Mines produced an estimated 20,510 tonnes of nickel in 2023, while the Sudbury Area Mine contributed approximately 18,590 tonnes.

Canada Nickel Company (TSXV: CNC, OTCQX: CNIKF) is emerging as a significant player in the North American nickel industry with its flagship Crawford project in Ontario. The project is the largest nickel reserve in North America and expects to become the largest nickel sulfide operation in the Western world when fully operational.

The company's focus on producing "clean, green nickel" positions it well to meet the growing demand from the electric vehicle and stainless steel markets.

FPX Nickel (TSXV: FPX, OTCQB: FPOCF): is a Vancouver-based junior nickel mining company developing the large-scale Decar Nickel District in central British Columbia. The company's Baptiste Project is projected to be among world’s ten largest nickel mines by annual output, with a focus on low carbon mining (2.4 t CO2/t Ni).

In 2023, FPX Nickel was one of the first companies to receive direct funding (of $725,000) for mining under Canada's critical mineral strategy, to accelerate demonstration of nickel sulphate production for the electric vehicle battery supply chain. And, in 2024, the company received $14.4M strategic equity investment from major nickel producer Sumitomo Metal Mining.

In October 2024, the company successfully completed a pilot-scale hydrometallurgy refinery testwork and produced battery-grade nickel sulphate from its Baptiste Nickel Project.

Aston Minerals (ASX:ASO) is a development phase mining company, advancing its flagship Edleston Project in Ontario, Canada. The company's Boomerang nickel-cobalt sulphide deposit boasts a substantial resource of 1.044 billion tonnes grading 0.27% nickel and 0.011% cobalt, making it one of the world's largest undeveloped nickel-cobalt sulphide deposits.

The team brings extensive experience from successful ventures, selling 10 mining projects globally, including the 85,000tpa nickel producer LionOre, which was acquired by Russia’s Norilsk in 2007 for $US6.4 billion.

Lundin Mining Corporation (TSX: LUN) operates the Eagle Mine in Michigan's Upper Peninsula, one of the few primary nickel mines in the US. The underground mine, acquired from Rio Tinto in 2013, produces nickel and copper concentrates. With a production capacity of approximately 2,000 tonnes per day, Eagle Mine is a crucial domestic source of nickel for the U.S. market.

Lundin Mining's continued investment in the Eagle operation underscores the strategic importance of maintaining domestic nickel production capabilities in North America.

Talon Metals Corp. (TSX: TLO, OTC: TLOFF) is advancing the high-grade Tamarack Nickel-Copper-Cobalt Project in central Minnesota, in partnership with Rio Tinto. The company has secured significant support from the US Department of Defense, securing a US$20.6 million grant to accelerate exploration in Minnesota and Michigan.

With an agreement to supply 75,000 metric tonnes of nickel concentrate to Tesla, Talon is well-positioned to capitalize on the growing demand for battery minerals in North America.

Conclusion

Securing supply chains are now a strategic imperative for North America’s national security — and this includes nickel — and time to develop new supply is running short. For investors, this is a compelling opportunity.

Disclaimer

The Oregon Group maintains full editorial control over all content published on this website. While sponsored and advertised placements may be featured, the content remains the sole opinion of The Oregon Group. The author may receive compensation or remuneration for providing content, but all statements and expressions are made independently and are not influenced by sponsors or advertisers. From time to time, The Oregon Group and its directors, officers, partners, employees, authors, or members of their families, as well as persons who are interviewed for articles on this website, may have a long or short position in securities or commodities mentioned and may make purchases and/or sales of those securities or commodities in the open market or otherwise. By accessing and using this website, readers are cautioned to assume that each of the foregoing persons may have a financial interest in all companies and sectors mentioned on this website. Any projections, market outlooks or estimates herein are forward looking statements and are inherently unreliable., and any such statements are based upon certain assumptions and should not be construed to be indicative of the actual events that will occur. Other events that were not taken into account may occur and may significantly affect the returns or performance of the securities or commodities discussed herein. The information provided herein is based on matters as they exist as of the date of preparation and not as of any future date, and The Oregon Group undertakes no obligation to correct, update or revise the information in this document or to otherwise provide any additional material. The information provided on this website is for informational purposes only and is not, directly or indirectly, an offer, solicitation of an offer and/or a recommendation to buy or sell any security or commodity, and the information provided on this website should not be construed as any advice or an opinion as to the price at which the securities of any company or commodity may trade at any time. The Oregon Group is a publisher of financial information, not an investment advisor. We do not provide personalized or individualized investment advice or information that is tailored to the needs of any particular recipient, and the information provided on this website is not and should not be construed as personal, financial, investment or professional advice. Readers are cautioned to always do their own research and review of publicly available information and to consult their professional and registered advisors before purchasing or selling any securities or commodities and should not rely on the information contained herein. Neither The Oregon Group nor any of its affiliates accepts any liability whatsoever for any direct or consequential loss howsoever arising, directly or indirectly, from any use of the information contained herein. By using the Site or any affiliated social media account, you are indicating your consent and agreement to this disclaimer and our terms of use. Unauthorized reproduction of this newsletter or its contents by photocopy, facsimile or any other means is illegal and punishable by law.

Read more on The Oregon Group: Nickel mining in North America: it’s a US national security issue